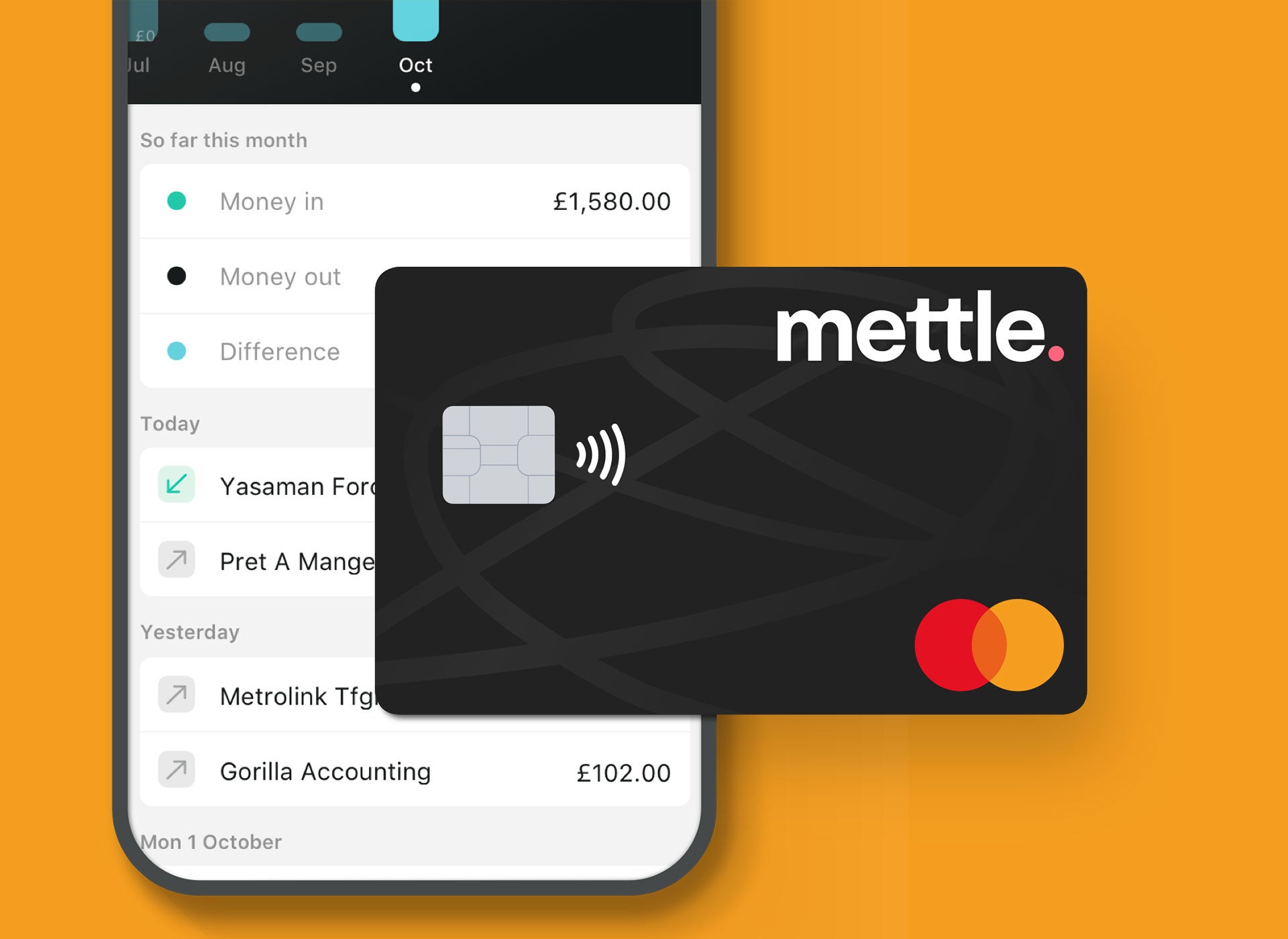

Mettle is a standalone digital-only business bank launched by Natwest that focuses on sole traders and limited companies with up to two owners. Image courtesy of Mettle.

Mettle is a standalone digital-only business bank launched by Natwest that focuses on sole traders and limited companies with up to two owners. Image courtesy of Mettle.

With the closure of numerous bank branches around the UK as a result of lockdown measures, as well as a rapid shift online as remote working becomes the norm for many, it would be easy to assume that digital banking has fared well during the Covid-19 pandemic.

However, like virtually every industry, the UK’s world-renowned fintech sector has encountered its fair share of ups and down over the past few months.

According to research by software company Qadre, 68% of fintech founders reported missing out on funding as a result of the Covid-19 crisis, amounting to as much as £2.6bn.

According to Sifted, Monzo, Revolut, Starling and N26 saw their growth rate drop by between 18% and 36% in their native markets.

However, as one of the fastest growing sectors in the UK, fintech is in a better position than many other industries to bounce back.

Different approaches: Natwest launches Mettle

One brand new to the UK fintech space is Mettle. Soft launched by Natwest in September 2019, Mettle is a standalone digital-only business bank focused on sole traders and limited companies with up to two owners offering features such as invoicing, book keeping, and tools to help small businesses be “tax ready”.

Verdict spoke to Mettle’s chief product officer Ken Johnstone, who explains that his involvement in Mettle comes out of his own past frustrations of banking as a startup.

“I’ve done a couple of startups in the past and one of the things you do when you start a business is you open a bank account and I chose the bank that I did my personal banking with as many people do, you just gravitate to what you know,” he says.

“It was one of the big highstreet banks, but the experience of getting up and running was horrendous. I had to physically go to a bank on four different occasions with ID, with signed physical paperwork and the whole experience took quite a few weeks just to get up and running. But with products like Mettle I can get up and running straight away essentially if my business profile is acceptable. So that is a problem for all big banks that they need to solve. We might see different approaches to that.”

The narrative surrounding the rise of digital banking has often focused on incumbents versus challengers, with it increasingly obvious that traditional banks must step up their customer offerings in order to compete with newer and more digitally-savvy startups and remain relevant to today’s customers.

Faced with the hurdle of legacy systems and traditional ways of working some have opted to launch independent digital brands.

In February, American investment bank JP Morgan announced that it will be launching a digital bank in the UK.

This has not always been entirely successful, with the news that RBS’s digital banking brand was closing customer accounts and “winding down” after just six months

However, Johnstone explains that in such a new industry, trying new things can sometimes mean some products fall by the wayside:

“I view [Bo’s closure] as Natwest trying a few innovative things, and I view it as a big AB test. It’s product mentality but when you want to try things, you try a couple of things, you watch what’s working best and you double down on it. You focus on it to give it the best chance of success. It demonstrates that way of thinking and the reality is in business banking, there is a little revolution happening and that’s amplified by what’s happening at the moment. I guess the view was there’s a bigger opportunity in business banking so let’s focus there.”

The best of both worlds

The past few years have seen the meteoric rise of fintech startups such as Monzo and Starling, leaving some to question how traditional banks can compete with agile startups. Johnstone explains that operating as an independent brand serving a specific business community while having links to a well-known brand such as Natwest gives Mettle “the best of both worlds”.

“Certainly there are segments that like a higher touch approach that those bigger banks can offer. From our point of view the customers that we’re dealing with probably are closer to the customers that Monzo and Starling are dealing with who are happy with the lighter touch approach. They just want an efficient, great user experience and they want good value and from our point of view we’re definitely closer to the Monzos and the Starling but I see Natwest as a bit of an unfair advantage because it gives us the best of both worlds,” he says.

“We run completely independently and if you look at the makeup of the team at Mettle, yes, there are some people have been working in banking for a long time but there are a lot of other people who are either from fintechs or have done other types of startups or other types of B2B businesses or consumer businesses and it’s definitely a different way of working. So we’re run independently, we can be agile we can br nimble, we can have quite a lean approach to what we do, try things with customers. But we have that Natwest connection where there’s a lot of experience and a lot of learnings, some of which have been pretty tough learnings over the years, that we can draw on…our customers can feel confident that behind Mettle there is a big banking institution and that their finances are secure.”

Through its link to the Natwest group, Mettle is able to offer customers access to Free Agents accounting software free of charge, and Johnstone believes that this ability to leverage assets such as this while remaining independent is what “sets the brand apart”.

Small business banking

Small businesses have unsurprisingly been affected by the pandemic, with a survey from Simply Business survey showing that the pandemic has cost UK small businesses over £11,000 on average. This may not seem like much, but for the “writers, photographers, designers,engineers, handymen and dog walkers” that Mettle serves, this can be the difference between survival and closure.

In April the UK government launched the The Small Business Grant Fund, with small businesses entitled to a one-off cash grant of £10,000 from their local council. The British Business Bank also recently approved three challenger banks to deliver the Coronavirus Business Interruption Loan Scheme.

Johnstone explains that, especially in the current climate, small businesses have specific banking needs that are not always met by larger traditional banks.

“The view is that the smaller end of businesses, so freelancers, contractors, very small limited companies, project workers etc. have been really caught between retail and business banking for a long time,” he says.

“Business banks, the big traditional banks including Natwest and the others, have focused more on larger businesses and enterprises, so there’s been this gap in the market where people have been using personal accounts for business purposes, for very basic banking, but we felt there was an opportunity to do something completely new, completely digital on a new tech stack and offer a lower cost digital only focused offering.

“It’s about getting up and running, getting a simple view of my finances and not having to worry about financial matters. The customers we speak to want to be running their businesses. They want to be, marketing, doing sales developing product themselves and not worrying about finances.”

“A catalyst and an opportunity to do something new”

Mettle itself, explains Johnstone, has been impacted by the events of the last few months, despite being owned by Natwest, but is now experiencing a “steady recovery”:

“I think every industry has been affected. We definitely saw a drop in engagement between February and March we probably saw around a 20% drop in engagement across the board and by that I mean transactions in, transactions out and usage of other features like invoices for example,” he says.

“Customers were invoicing less which would suggest that they had been impacted. That said, it’s pretty much back to where it was. We’ve seen a steady recover over the last six to eight weeks. If we’re not already where we were we’re very close to.”

Although much of the reporting around the financial impact on the pandemic has focused on the negative impacts it has had on business, Johnstone believes that there have also been some positives:

“There’s a new normal emerging as we know. A couple of dynamics that we see really strongly, the first one is a lot of businesses are struggling, they’ve kind of going into survival mode and it’s all about getting through the year and adapting to a new normal and adapting to potentially having to deal with customers remotely,” says Johnstone.

“That’s one dynamic and the other one is a lot more positive in that we’re also seeing a lot of people taking the plunge. I was looking at stats yesterday for general business formation and in June 2020 compared to June 2019 there’s about a 20% uplift in businesses being formed. A lot of those are freelancers, contractors and temporary workers, but there is definitely a segment where people have either been forced to through being furloughed or losing their jobs, or just seeing a catalyst and an opportunity to do something new, something a bit different.”

Read more: Digital bank Bo closes: Inside RBS’s failed challenge to the challenger banks.

Global Construction Outlook to 2024 (COVID-19 Impact)

Our parent business intelligence company